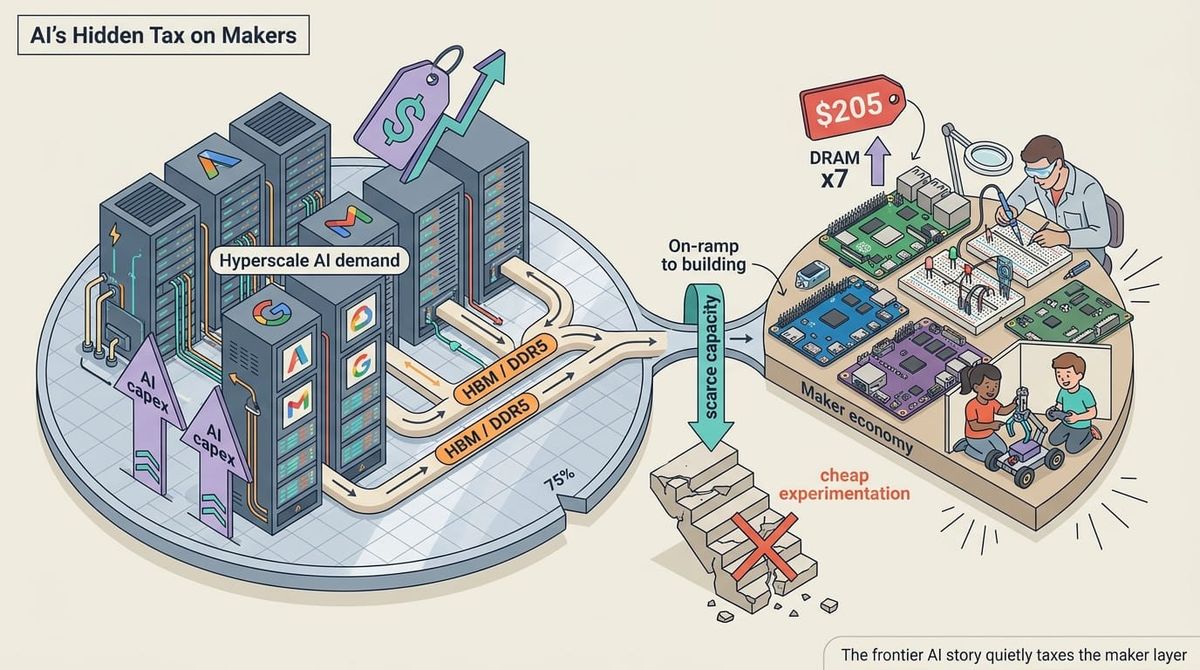

AI's Hidden Tax on Makers

I assumed the maker renaissance ran on its own track, insulated from the frontier AI story. The price of a Raspberry Pi proved it's downstream of the same demand.

For the last few years I've watched two AI stories run on separate tracks. One is the trillion-dollar hyperscale story: training runs, GPU clusters, data centers the size of small cities. The other is the quiet, cheap one: a fifty-dollar board running a small vision model at the edge, a sensor rig in someone's garage, a retired engineer prototyping an idea before it ever touches a production budget. I assumed that second track was a separate universe. Different economics, different customers, different risk. I was wrong, and the proof showed up in the price of a Raspberry Pi.

The Price Hikes

Raspberry Pi raised prices twice in the first four months of 2026. The first hike landed February 2, adding as much as $60 to Pi 4, 5, and Compute Module variants with 2GB of memory or more. The second landed April 1, and it was worse: the 16GB Pi 5 jumped $100 to $205, and the Pi 500+ kit rose $150. That flagship board now costs about 70 percent more than its original list price. The company was direct about why: LPDDR4 memory, the DRAM used in the Pi 4 and 5, is up roughly sevenfold in a year.

The Real Cause

That number is the whole story, and it has nothing to do with Raspberry Pi as a company. Samsung, SK Hynix, and Micron, the three firms that make almost all the world's DRAM, are reallocating fab capacity away from ordinary memory and toward high-bandwidth memory and enterprise DDR5, the chips that go into AI training and inference hardware. Data centers now account for an estimated 70 percent of memory chips produced worldwide. Analysts describe this as a structural reallocation of global fab capacity, not a cyclical shortage that clears in a quarter. Samsung and SK Hynix have both said the crunch could run into 2027 and beyond.

Same Silicon, Same Story

So the assumption breaks down at the level of the wafer. A fifty-dollar maker board and a frontier training cluster are drawing from the same finite pool of silicon capacity, and the buyer with the bigger budget wins the allocation every time. The maker economy is part of the same AI capex story, just the part with no seat at the table when the fabs decide who gets served first.

The Harder Question

Here's the harder question I keep circling, and it's the one worth sitting with longer than the price-hike headline. What value do builders actually bring to the market that we stand to lose if this keeps squeezing them out? Is the maker layer a nice-to-have that the market is correctly pricing out of existence, or is it something load-bearing?

I don't have a clean answer. But I think the honest version splits the question in two. The casual experimenter, the person who was one impulse order away from trying something, gets priced out when the board that cost $80 now costs $205. That's a real, if invisible, loss: fewer weird little projects that never had a business case to begin with, just curiosity. The committed builder doesn't disappear the same way. They route around the tax: a Pi Zero, a microcontroller that never needed this much memory to begin with, a used unit off the secondhand market. They pay in time and friction instead of dollars.

The Real Cost

So maybe the real casualty of a DRAM shortage isn't the builder economy itself. It's the on-ramp into it, the cheap, disposable tinkering that turns a curious person into a committed one. The maker layer is where that happens, where the test runs before anything becomes a business or a deployment: the plumber prototyping a fabricated part on a cheap board, the parent building a sensor project with a kid, the practitioner testing a home automation agent before proposing anything like it inside a large organization. All of them are running live experiments where judgment meets tooling at a price point that made experimentation close to free. That's the loss I'd actually worry about.

Scarcity Breeds Resourcefulness

There's a more interesting read, too. Scarcity tends to make builders resourceful in ways worth watching. If the 16GB Pi 5 is priced like a mid-range laptop, the energy migrates toward the boards nobody was paying attention to: a Pi Zero doing one job well, or a community forming around the Orange Pi 5 Plus or Rock 5B because that's what's actually in stock. None of those boards escape the same DRAM curve. But where builders route around a shortage usually tells you more than what the shortage stops.

The Alternatives

So what are the actual alternatives, not the romantic ones? Raspberry Pi itself protected its lowest tier: the 1GB boards, the Pi Zero, and the Pi 3 ride on older LPDDR2 memory the company still holds years of inventory in, so the true entry point survives, just capped in capability. On the higher end, boards like the Orange Pi 5 Plus, Radxa Rock 5B, and Banana Pi M7 share the same Rockchip RK3588 silicon and outperform the Pi 5 on raw compute. But you're trading a decade of Raspberry Pi's mainline kernel support, documentation, and community troubleshooting for a rougher stack, thinner NPU driver support, and forum threads instead of official docs. And none of these boards escape the underlying DRAM curve. The relief is regional and temporary, not structural.

The Ecosystem Tax

That relief is conditional either way. A lot of what you're actually paying for with a Pi isn't the silicon, it's a decade of HATs, GPIO conventions, mainline kernel support, and a Stack Overflow answer for every mistake you're about to make. Drop to a Pi Zero or jump to an Orange Pi and you're not just changing chips, you're leaving that ecosystem behind, and for a lot of projects the ecosystem was the actual product.

The Practical Move

The practical move, if you're speccing an edge or sensor project on a tight margin, is to stop treating memory as a fixed line item in your bill of materials and start treating it as a volatile commodity. Spec down deliberately where the project allows it. The 2 to 4GB tier is where this shortage bites least, and where the maker economy still has room to keep experimenting cheaply enough to matter.

The Bottom Line

The frontier AI story and the maker story were never separate. One is quietly taxing the other, and the bill is arriving as a line item on a fifty-dollar board.